I’ve spent years helping expats understand car insurance in Hong Kong. The process taught me something valuable: when you understand exactly what you’re buying, you can make informed decisions that save you thousands whilst ensuring proper protection.

The financial opportunities are substantial. Understanding how premiums are calculated based on vehicle values can help you optimise your coverage. Knowing how to transfer no-claims discounts earned abroad can save you 30-50% annually. Understanding cross-border coverage options opens up Greater Bay Area travel. Knowing how excess charges work helps you budget accurately.

Car insurance in Hong Kong has specific features that differ from other markets. Premium calculations, coverage limits, deductibles, and documentation requirements all have local characteristics. Understanding these helps you make better purchasing decisions.

Let me show you what you need to know.

1. Understanding Estimated Value vs Market Value

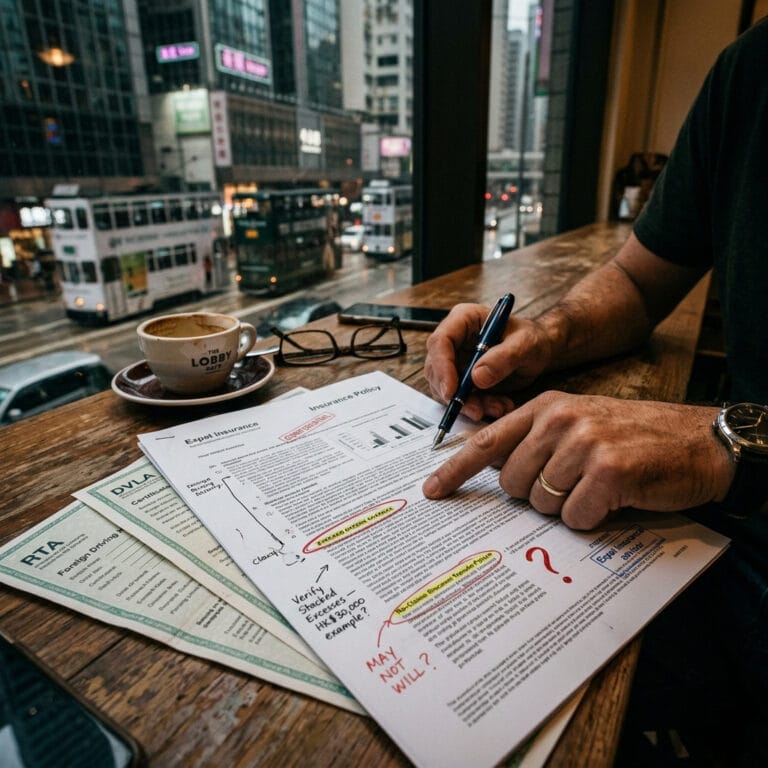

When expats come to me about car insurance in Hong Kong, one of the most important concepts to understand is the difference between “estimated value” and “market value”.

Your car insurance policy lists an estimated value for your vehicle. Let’s say it shows HK$300,000. This figure serves an important purpose in your policy structure.

Here’s what you need to know:

When a total loss occurs, insurers assess and pay based on “current market value at the time of loss”—not the estimated value listed on your policy. The estimated value serves as a maximum ceiling, whilst market value determines actual payout, ensuring you don’t pay too much for your car insurance.

How does this structure work?

The estimated value functions as a cap on the insurer’s liability. They’ll never pay more than this amount, but the actual payout is based on market value at the time of your claim. Market value means the cost of replacing the insured car with one of the same make and model, of similar condition, specification and age as prevailing immediately before the accident.

Understanding this distinction helps you make informed decisions about your car insurance in Hong Kong coverage.

Your premium calculation incorporates the estimated value, whilst your potential payout will be based on the lower market value. This is standard practice across car insurance in Hong Kong providers.

Here’s where car insurance in Hong Kong gets more nuanced.

If at the time of a claim the insurer finds that you’ve under-insured your vehicle—insured a sum lower than the actual market value—then the clause of “Average” will be applied. The claimable amount will be reduced by the same proportion of under-insurance.

Conversely, if at the time of a claim the insurer finds that you’ve over-insured the vehicle, the maximum claimable amount will still only be the market value including depreciation and minus the excess where applicable. The insurance is designed to restore you to your pre-accident position, not to provide profit.

Understanding this helps you choose the right insured value for optimal car insurance in Hong Kong coverage.

2. How Car Insurance in Hong Kong Premiums Are Calculated

The estimated value represents only a small part of how car insurance in Hong Kong premiums are calculated. Insurers have their own formulas and data to determine pricing. This explains why you can get different quotes for the same vehicle and driver from different insurers.

The variation can be significant.

Industry research reveals that identical coverage quotes for the same vehicle can vary substantially between insurers—sometimes differing by 50% or more for identical risk profiles.

Different insurers have different claims experience on certain vehicle types and driver profiles. Understanding this variation helps you shop effectively for car insurance in Hong Kong coverage.

This pricing variation in car insurance in Hong Kong isn’t specific to expats. It affects all drivers. But expats face an additional consideration that local drivers may not encounter.

3. Transferring Your Overseas No-Claims Discount

You’ve driven claim-free for ten years in your home country. You arrive in Hong Kong with documentation proving your excellent driving record. Understanding how to transfer this history to your car insurance in Hong Kong premium can save you thousands.

Here’s what you need to know about No-Claims Discount (NCD) transfer.

Some insurers in Hong Kong won’t recognise an NCD from overseas insurers. Others will accept overseas NCD subject to documentation requirements. The NCD gives you a percentage discount on your car insurance premium for each additional year if you fulfil the specified conditions, though eligibility may differ from insurer to insurer.

Insurers that accept overseas NCD typically require specific documentation.

You’ll need current certificates (not several years old), in English or Chinese, from your previous insurer. The documentation should clearly show your claims history and the period of insurance.

The important detail: policies typically state expatriates “may” transfer foreign NCD with proper documentation, subject to approval. This means preparing the right paperwork before arriving in Hong Kong increases your chances of recognition.

Successful NCD transfer can save you 30-60% on your car insurance in Hong Kong premiums.

The financial benefit is substantial. NCD can save up to 60% on premiums, making it one of the most valuable benefits for drivers purchasing car insurance in Hong Kong. With proper documentation, your overseas driving history can translate directly into premium savings. For a comprehensive policy on a mid-range vehicle, this could mean saving several thousand Hong Kong dollars annually.

4. Cross-Border Coverage for Greater Bay Area Travel

Many expats in Hong Kong regularly drive to Mainland China or Macau. Weekend trips to Shenzhen. Business meetings in Guangzhou. Family holidays across the Greater Bay Area.

Standard comprehensive car insurance in Hong Kong policies typically exclude coverage outside Hong Kong’s territory.

This is important to understand.

Your comprehensive car insurance policy—the one you’re paying for—may not cover you the moment you cross into Mainland China unless you’ve arranged additional coverage.

Under the Motor Vehicles Insurance (Third Party Risks) Ordinance, Chapter 272 of the Laws of Hong Kong, the user of a motor vehicle on the road must insure liability for death or bodily injury of third parties with an authorised insurer. This requirement applies to Hong Kong territory. For Mainland travel, different arrangements are needed.

For expats who regularly travel to the Mainland, understanding how to extend your car insurance in Hong Kong coverage across borders is essential.

The Hong Kong Government, Insurance Authority and Mainland authorities reached an agreement for implementing Unilateral Recognition policy, comprising a main Hong Kong car insurance cover and a top-up Mainland cover issued by a Hong Kong insurer, so car owners don’t have to purchase two separate policies. However, not all insurers participate in this scheme, so checking with your car insurance in Hong Kong provider about cross-border options is essential.

The same principle I apply to medical insurance applies here: understand your geographical coverage before you need it, not after an incident occurs.

5. Understanding How Excess Charges Work

Excess terms represent an important aspect of car insurance in Hong Kong that affects your out-of-pocket costs when making a claim.

Most car insurance policies have an excess, which is the initial amount of any claim that you must meet yourself, with the amount varying depending on types of claims and whether the accident is caused by a named or unnamed driver.

Consider this scenario: You have a HK$40,000 claim involving an unnamed, young, inexperienced driver. Your total excess could comprise:

-

HK$5,000 general excess

-

HK$5,000 unnamed driver excess

-

HK$10,000 young driver excess

-

HK$10,000 inexperienced driver excess

You might have HK$10,000 to HK$30,000 in combined excess on a HK$40,000 claim, depending on your policy terms.

Besides unnamed driver excesses, young and inexperienced driver excesses are common excesses, with ‘young driver’ usually referring to drivers under 25 years of age, whilst ‘inexperienced driver’ refers to drivers who have held a driving licence for less than 2 years. Understanding how these combine in your car insurance in Hong Kong policy helps you budget for potential claims.

6. Depreciation and Betterment in Claims

Beyond the basic excess, there’s another aspect of car insurance in Hong Kong claims to understand: depreciation when calculating the claimable amount for own-damage. This can also be referred to as “betterment”.

The concept works like this: new replacement parts and repairs to your damaged vehicle can actually increase the overall market value of your vehicle. This “betterment” amount may be deducted from the claimable amount.

The practical impact: the claimable amount for own-damage repairs will typically be the repair cost minus the excess minus any applicable depreciation.

This is standard practice amongst car insurance in Hong Kong providers for claims for own-damage. Understanding this multi-layer calculation helps you set realistic expectations for claim settlements.

7. What “Comprehensive” Actually Covers

“Comprehensive” car insurance in Hong Kong provides extensive coverage, but understanding what’s included and excluded helps you make informed decisions.

Comprehensive motor insurance covers third-party liabilities and medical expenses of the insured in an accident, and also includes repairs, non-collision damage and theft. However, standard policies have geographical limitations and specific exclusions.

Most importantly, mechanical or electrical breakdowns or failures are typically not covered by car insurance in Hong Kong policies.

As with all insurance policies, car insurance policies have exclusions for which the insurance will not pay a claim, so always checking your policy carefully is essential, with common exclusions including use of vehicles outside the specified geographical area and damage caused because a driver was unlicensed, drunk or under the influence of drugs.

I apply the same principle to car insurance in Hong Kong that I use for medical insurance: understand what you’re covered for and what exclusions apply before you need the coverage.

Under Hong Kong law, it is mandatory for all motor vehicle owners to take out insurance that covers third-party liabilities of at least HK$100 million for bodily injury or death and HK$2 million for property damage. Under the Motor Vehicles Insurance (Third Party Risks) Ordinance, it is compulsory to take out insurance with an authorised insurer to cover your liabilities for injury or death of third parties arising out of the use of your motor vehicle. But third-party policies explicitly exclude coverage for the driver’s own death, injury, or vehicle damage.

Expats purchasing the legally required minimum coverage should understand that third-party car insurance in Hong Kong protects others from you, but doesn’t cover your own vehicle damage or injuries.

8. NCD Protection: Benefits and Limitations

Some car insurance in Hong Kong providers offer “NCD Protection” coverage. This can be valuable for drivers who want to preserve their no-claims discount.

Understanding how the protection works helps you evaluate its value.

Under No Claim Discount Protection, if the sum of all your claims during the current period of insurance does not exceed HK$60,000 or 20% of your car’s reasonable market value (whichever is lesser), you will be entitled to the same NCD as under the policy at renewal. It applies to specific claim types and typically isn’t transferable to other insurance companies.

This portability consideration matters when choosing car insurance in Hong Kong.

The NCD protection can lock you into your current provider. If you want to switch insurers next year for better rates or coverage, you may lose the protection benefit. Understanding this trade-off helps you decide whether the protection is worth it for your situation.

9. The Motor Insurers’ Bureau Protection

An important but often overlooked aspect of car insurance in Hong Kong is the Motor Insurers’ Bureau (MIB) system.

The Motor Insurers’ Bureau of Hong Kong is a company incorporated in Hong Kong and limited by guarantee that provides compensation to victims of traffic accidents where the drivers concerned are uninsured or untraceable, or the insurers concerned are insolvent, with all motor insurance policies issued in Hong Kong contributing a surcharge based on the policy premium to MIB.

This surcharge appears on your car insurance in Hong Kong premium breakdown and provides an important safety net for all road users.

The regulatory framework in Hong Kong provides consumer protections. The Insurance Authority regulates insurers and intermediaries, whilst the Hong Kong Federation of Insurers issues codes of practice for the industry.

Understanding your rights and the regulatory protections helps you navigate the car insurance in Hong Kong market with confidence.

10. Making Informed Car Insurance in Hong Kong Decisions

I’ve spent years helping expats understand medical insurance because the stakes are too high to rely on assumptions. Quality healthcare doesn’t come cheap, and neither does proper car insurance in Hong Kong coverage.

The same principles apply to both:

Understand what you’re buying before you need it. Don’t wait until you’re filing a claim to discover what’s excluded from your car insurance in Hong Kong policy.

Compare coverage, not just premiums. The cheapest car insurance in Hong Kong quote often comes with the most restrictive terms. Given the premium variation between insurers for identical coverage, comparison is essential.

Document everything. If you want your overseas NCD recognised in your car insurance in Hong Kong policy, obtain current certificates in English or Chinese before you arrive. Don’t assume documentation from years ago will suffice.

Ask about cross-border coverage explicitly. If you drive to Mainland China or Macau, arrange extended car insurance in Hong Kong coverage before your first trip, not after an incident occurs.

Understand how excess charges combine. Ask your car insurance in Hong Kong provider or broker to provide examples of total excess for different claim scenarios, particularly if you have young or inexperienced drivers who might use your vehicle.

Read the total loss settlement terms. Confirm whether your car insurance in Hong Kong payout will be based on estimated value, market value, or some other calculation method.

Evaluate the value of NCD protection. If it locks you into one insurer, calculate whether the car insurance in Hong Kong protection benefit is worth sacrificing portability and competitive pricing.

Why Understanding Car Insurance in Hong Kong Matters

In medical insurance, I help expats understand healthcare costs so they can make informed decisions about the limits they buy. The same approach applies to car insurance in Hong Kong.

You need to understand what protection you’re actually purchasing, what exclusions apply, and what financial exposure remains despite your coverage.

Car insurance in Hong Kong has specific features worth understanding: how premiums are calculated, how coverage limits work, what documentation is needed for NCD transfer, and how cross-border coverage operates. Understanding these features helps you make better purchasing decisions and ensures you have appropriate protection.

Knowledge is power when it comes to car insurance in Hong Kong.

At Expat Insurance, we’re compensated by insurance companies directly, which means the coverage reviews and advice we offer you cost nothing. The car insurance in Hong Kong premiums we quote are identical to those offered by insurance companies to direct buyers. But our value comes from understanding your needs, explaining what coverage actually means, and helping you make informed decisions about your protection.

We do this for medical insurance because expats deserve clear explanations and comprehensive advice. The same principle applies to car insurance in Hong Kong.

If you’re purchasing or renewing car insurance in Hong Kong coverage, don’t rely on assumptions. Ask questions. Compare coverage, not just premiums. Understand what you’re covered for and what exclusions apply.

And if you need help making sense of policy terms, excess structures, or cross-border coverage options for your car insurance in Hong Kong needs, that’s what we’re here for.

With the right information, you can select car insurance in Hong Kong coverage that provides proper protection at a fair price.

How You Get The Car Insurance in Hong Kong Protection You Need

Car insurance in Hong Kong doesn’t have to be complicated. At Expat Insurance, we help you understand exactly what you’re buying and make sure your policy protects what matters most to you.

No pushy sales tactics. We have a friendly conversation, show you the lay of the land, and explain the different car insurance in Hong Kong options available. You move forward at your own pace. People choose to work with us because we educate them on their options and help them feel confident about what will work best for them.

We’ll walk you through the estimated value versus market value distinction so you understand total loss settlements. We’ll explain the excess structure so you know what you’ll pay out-of-pocket for different claim scenarios. And we’ll help you navigate the NCD documentation requirements and cross-border coverage extensions, whether you’re driving a family saloon in Hong Kong Island or travelling to Guangdong regularly.

Our goal is straightforward. We want you to have car insurance in Hong Kong coverage that works when you need it.

Get in touch with us today. We’ll review your car insurance in Hong Kong situation, answer your questions, and help you find a policy that provides the protection you need at a price that makes sense.

How We Work With You

Our process is straightforward and designed around your needs.

Step 1: We Talk and Answer Your Questions

When you get in touch, we’ll get back to you for a friendly conversation. We’ll explain who we are, what we do, and most importantly, what we’re going to do for you specifically. We’ll answer any questions you have about car insurance in Hong Kong.

Step 2: We Educate You on Your Options

We’ll research the car insurance in Hong Kong market and come up with quotes and options tailored to your situation. Whether you need third-party coverage, comprehensive protection, or cross-border extensions for Mainland China travel, we’ll find insurers willing to provide the coverage you need. We’ll take you through each car insurance in Hong Kong option so you understand what’s available.

Step 3: You Decide What Works Best

As required we’ll meet with you in person, speak on the phone or video call, or email to discuss your car insurance in Hong Kong options. We’ll explain the differences between policies, help you understand the excess structures, clarify the estimated value versus market value calculations, and make sure you’re comfortable with everything. The choice is yours. We’re here to help you make an informed decision about your car insurance in Hong Kong coverage.

Step 4: We Stay With You

Once your car insurance in Hong Kong policy starts, we’re here to help. We’ll contact you at least once a year to review your coverage, discuss any changes in your situation—new vehicles, additional drivers, increased cross-border travel to the Greater Bay Area—and consider any additions you’d like to make. Your needs change over time, and your car insurance in Hong Kong should change with them.

Get in Touch With Us

Ready to find the right car insurance in Hong Kong coverage? We’re here to help you make an informed decision.

Contact us today:

Website: https://expatinsurance.com.hk/contact/

Phone: +852 3563 9771

Office Location: Suite 701, Connaught Commercial Building, 185 Wan Chai Road, Wan Chai, Hong Kong

Email: [email protected]

Whether you’re new to Hong Kong or renewing your existing car insurance, we’ll help you understand your options and find coverage that protects what matters most.

Sources

This article references information from the following authoritative Hong Kong sources:

Disclaimer: Whilst we strive to reference accurate and authoritative sources, insurance regulations, policy terms, and web content may change over time. Some linked content may become outdated or unavailable. For important car insurance in Hong Kong decisions, please always contact us directly for current information and personalised advice tailored to your specific situation.