I’ve spent years helping expats understand motor insurance in Hong Kong. The process taught me something valuable: understanding what you’re buying makes all the difference in getting the protection you need.

Motor insurance in Hong Kong has unique features that every expat should know about before purchasing a policy.

Here’s what I mean.

Understanding Estimated Value vs. Market Value

When expats come to me after purchasing motor insurance, there’s one concept that’s worth clarifying right from the start: what “estimated value” actually means for your coverage.

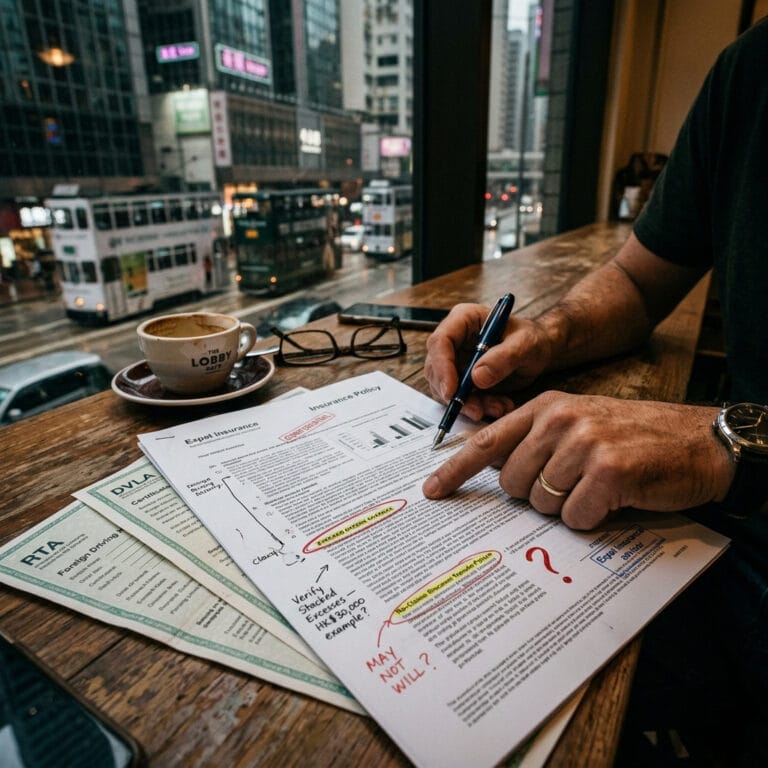

Your policy lists an estimated value for your vehicle. Let’s say it shows HK$300,000. You see that number and assume that’s what you’ll receive if your car is written off in an accident.

Here’s what you need to know.

When a total loss occurs, insurers assess and pay based on “current market value at the time of loss”—not the estimated value listed on your policy. The estimated value serves as a maximum ceiling for payouts.

Here’s how this works:

The estimated value functions as a cap on the insurer’s liability. The market value at the time of your claim determines the actual payout, and that figure can be significantly lower than the estimated value shown on your policy schedule.

When I explain this distinction to expats, they always want to understand more about how it works.

The key point is that your premium calculation takes the estimated value into account, whilst your payout will be based on the market value. Understanding this difference helps you make informed decisions about your coverage.

But here’s where motor insurance gets more complicated.

Why Motor Insurance Premiums Vary Between Insurers

The estimated value represents only a small part of how premiums are calculated. Insurers use their own formulas and claims data to determine pricing. This explains why you can get significantly different quotes for the same vehicle and driver from different insurers.

The variation can be substantial.

A 2024 study revealed identical coverage quotes for the same Toyota Camry ranged from HK$4,200 to 7,100 – a 69% variation between insurers for identical risk profiles.

Different insurers have different claims experience on certain vehicle types and driver profiles. The premium variations can be significant—I’ve seen premiums differ by double or more from one insurer to another for the exact same risk.

This premium variation in motor insurance isn’t specific to expats—it affects everyone. But expats do face an additional consideration that’s worth understanding.

Transferring Your No-Claims Discount to Hong Kong

You’ve driven claim-free for ten years in your home country. You arrive in Hong Kong with documentation proving your excellent driving record. Naturally, you’d expect this history to benefit your Hong Kong motor insurance premium.

Here’s what you need to know about NCD transfer.

Some insurers accept No-Claims Discount (NCD) from overseas insurers, whilst others have policies that only recognise NCD from local Hong Kong insurance providers.

Even insurers that accept overseas NCD have specific documentation requirements that you’ll need to meet.

Common documentation issues include: no documentation provided, certificates that are several years old, or paperwork in languages other than Chinese or English.

The most important thing to know: even with current documentation in English or Chinese from a reputable overseas insurer, not all Hong Kong insurers will recognise it. Some expats start with zero discount despite years of claim-free driving abroad.

The financial impact is worth considering. Without NCD recognition, premiums can be 30-50% higher. For a comprehensive policy on a mid-range vehicle, that’s thousands of dollars annually—which makes understanding the NCD transfer process essential.

What You Need to Know About Cross-Border Coverage

Many expats in Hong Kong regularly drive to Mainland China or Macau. Weekend trips to Shenzhen. Business meetings in Guangzhou. Family holidays across the border.

Standard comprehensive motor insurance policies in Hong Kong typically have geographical limitations.[1] As MSIG explains, comprehensive coverage generally applies to “accidents that happen within the Hong Kong SAR” with accidental loss, damage or liability outside Hong Kong generally excluded.

This is an important point to understand.

Your comprehensive policy provides coverage within Hong Kong. Once you cross into Mainland China, different coverage arrangements apply.

For own damage coverage in China, extended coverage can be arranged upon request.[5] For third-party liability insurance compliant with China regulations, separate coverage must be purchased. AXA notes that to drive into Guangdong through HZMB, “you are required to take out a valid statutory motor insurance” that meets Mainland regulatory requirements. These are optional extensions that you can add to your policy when travelling across the border.

I’ve seen similar patterns in medical insurance. The term “comprehensive” has specific meanings in insurance policies. Understanding what’s included—and what requires additional coverage—helps you make informed decisions.

The key difference is planning ahead. Knowing what coverage you need for cross-border travel lets you arrange appropriate extensions before your trip.

How Excess Charges Work: What Expats Should Know

Excess terms are an important aspect of your motor insurance coverage that’s worth understanding clearly.

You might see a policy with a HK$5,000 excess listed. It’s important to know that multiple excess charges can apply to a single claim, depending on the circumstances.

Consider this scenario: You have a HK$40,000 claim involving an unnamed, young, inexperienced driver. Your total excess could reach HK$30,000, comprising:

- HK$5,000 general excess

- HK$5,000 unnamed driver excess

- HK$10,000 young driver excess

- HK$10,000 inexperienced driver excess

You’re left with HK$10,000 claimable from a HK$40,000 claim—a 75% out-of-pocket burden.

Motor insurance policies list each excess type separately in the policy documents. Understanding how they combine in different claim scenarios helps you plan for your potential out-of-pocket costs.

Understanding What “Comprehensive” Motor Insurance Covers

“Comprehensive” motor insurance in Hong Kong provides extensive coverage, and it’s helpful to understand exactly what’s included.

Standard comprehensive policies have clearly defined coverage areas. They typically cover incidents within Hong Kong.[4] AXA’s comprehensive coverage includes “accident and third-party liability protection, along with multiple additional benefits” such as personal accident cover for the insured driver, windscreen replacement cover, and coverage for medical expenses. Policies also have standard exclusions including driving under the influence, unauthorised drivers, wear and tear, racing, and acts of terrorism.

Understanding these motor insurance coverage parameters helps you make informed decisions about what additional protection you might want to add.

I apply the same principle to motor insurance that I use for medical insurance: understand what you’re not covered for before you need the coverage.

The legal minimum in Hong Kong is third-party liability insurance[3] covering up to HK$100 million for bodily injury or death and HK$2 million for property damage. However, it’s important to understand that third-party policies specifically protect others from liability arising from your vehicle use—they don’t cover the driver’s own vehicle damage, injury, or death.

This is an important distinction: the minimum legal requirement protects third parties from your liability, whilst comprehensive coverage extends protection to you and your vehicle as well. Understanding this difference helps you choose the right level of coverage for your needs.

NCD Protection: What It Offers and What to Consider

Some insurers offer “NCD Protection” coverage as an optional add-on. This feature protects your no-claims discount even if you make a claim.

Here’s what you should know about how NCD protection works.

NCD protection typically has claim amount caps,[2] often not exceeding HK$60,000 or 30% of market value, whichever is lesser. It applies to specific claim types. One important feature: it’s generally not transferable to other insurance companies.

This portability aspect is worth understanding.

NCD protection is tied to your current motor insurance provider. If you want to switch insurers for different rates or coverage options, the protection doesn’t transfer with you. This means considering the trade-off between NCD protection and the flexibility to change insurers.

In medical insurance, we value portability highly. You benefit from the freedom to move between insurers as your needs change, as new products become available, or as pricing becomes more competitive. Understanding how NCD protection affects this flexibility helps you make the right choice for your situation.

7 Essential Tips for Expats Buying Motor Insurance

I’ve spent years helping expats understand medical insurance because the stakes are too high to rely on assumptions. Quality healthcare doesn’t come cheap, and neither does proper motor insurance.

The same principles apply to both:

Understand what you’re buying before you need it. Knowing your coverage details helps you avoid surprises when making a claim.

Compare coverage, not just premiums. The cheapest quote often comes with the most restrictive terms. Given the 69% premium variation between insurers for identical coverage, comparison is essential.

Prepare your documentation. If you want your overseas NCD recognised, obtain current certificates in English or Chinese before you arrive in Hong Kong. Current documentation gives you the best chance of recognition.

Plan for cross-border coverage. If you drive to Mainland China or Macau, arrange extended coverage before your first trip so you’re fully protected.

Understand how excess charges stack. Ask your motor insurance provider or broker to provide examples of total excess for different claim scenarios, particularly if you have young or inexperienced drivers who might use your vehicle.

Clarify total loss settlement terms. Confirm whether your payout will be based on estimated value, market value, or some other calculation method, so you understand what to expect.

Evaluate NCD protection carefully. If it limits your ability to switch insurers, consider whether the protection benefit outweighs the flexibility you’d be giving up.

Why This Matters

In medical insurance, I help expats understand healthcare costs so they can make informed decisions about the limits they buy. The same approach applies to motor insurance.

You need to understand what protection you’re actually purchasing, what exclusions apply, and what financial exposure remains despite your coverage.

Motor insurance in Hong Kong offers many options for expats. Understanding the key features of policies—coverage limits, deductibles, exclusions, and documentation requirements—helps you choose the right protection for your needs.

Knowledge makes all the difference.

At Expat Insurance, we’re compensated by insurance companies directly, which means the coverage reviews and advice we offer you are provided at no cost. The premiums we quote are identical to those offered by insurance companies to direct buyers. Our value comes from understanding your needs, explaining coverage options clearly, and helping you find the right protection for your situation.

We take this approach with medical insurance because expats benefit from clear explanations and comprehensive guidance. The same principle applies to motor insurance.

If you’re purchasing or renewing motor insurance in Hong Kong, taking time to understand your options makes a significant difference. Ask questions. Compare coverage, not just premiums. Know what protection you’re getting.

If you’d like help understanding policy terms, excess structures, or cross-border coverage options, we’re here to assist.

Making informed decisions about motor insurance protects you financially and gives you peace of mind on the road.

How You Get The Protection You Need

Motor insurance doesn’t have to be complicated. At Expat Insurance, we help you understand exactly what you’re buying and make sure your policy protects what matters most to you.

No pushy sales tactics. We have a friendly conversation, show you the lay of the land, and explain the different motor insurance options available. You move forward at your own pace. People choose to work with us because we educate them on their options and help them feel confident about what will work best for them.

We’ll walk you through the estimated value versus market value distinction so you’re not caught by the total loss payout gap. We’ll explain the excess structure so you know what you’ll pay out-of-pocket for different claim scenarios. And we’ll help you navigate the NCD documentation requirements and cross-border coverage extensions, whether you’re driving a family saloon or a performance vehicle.

Our goal is straightforward. We want you to have motor insurance coverage that works when you need it.

Get in touch with us today. We’ll review your motor insurance situation, answer your questions, and help you find a policy that provides the protection you need at a price that makes sense.

How We Work With You

Our process is straightforward and designed around your needs.

Step 1: We Talk and Answer Your Questions

When you get in touch, we’ll get back to you for a friendly conversation. We’ll explain who we are, what we do, and most importantly, what we’re going to do for you specifically. We’ll answer any questions you have about motor insurance.

Step 2: We Educate You on Your Options

We’ll research the motor insurance market and come up with quotes and options tailored to your situation. Whether you need third-party coverage, comprehensive motor insurance protection, or cross-border extensions for Mainland China, we’ll find insurers willing to provide the coverage you need. We’ll take you through each option so you understand what’s available.

Step 3: You Decide What Works Best

As required we’ll meet with you in person, speak on the phone / video call, or email to discuss your motor insurance options. We’ll explain the differences between policies, help you understand the excess structures, clarify the estimated value versus market value calculations, and make sure you’re comfortable with everything. The choice is yours. We’re here to help you make an informed decision.

Step 4: We Stay With You

Once your motor insurance policy starts, we’re here to help. We’ll contact you at least once a year to review your coverage, discuss any changes in your situation—new vehicles, additional drivers, increased cross-border travel—and consider any additions you’d like to make. Your needs change over time, and your motor insurance should change with them.

Ready to get the motor insurance coverage you need? Contact Expat Insurance today. We’ll take the time to understand your situation, explain your options clearly, and help you choose a policy that gives you the right protection at the right price. No pressure, no jargon—just straightforward advice from people who understand what expats need.

Get in touch:

Website: https://expatinsurance.com.hk/contact/

Phone: +852 3563 9771

Email: [email protected]

Office Location: Suite 701, Connaught Commercial Building, 185 Wan Chai Rd, Wan Chai, Hong Kong

Sources

This article draws on information and guidance from authoritative sources including Hong Kong insurance regulators, leading insurance providers, and consumer protection organisations:

- MSIG Insurance Hong Kong – Comprehensive Motor Insurance

- MSIG Insurance Hong Kong – Private Motor Car Insurance

- Investor and Financial Education Council (IFEC) – Motor Insurance

- AXA Hong Kong – AXA iMotor Insurance

- AXA Hong Kong – Motor Insurance for Hong Kong Private Cars Travelling to Guangdong

Important Disclaimer: Insurance policies, coverage terms, and linked content can change quickly and may become out of date. The information in this article and the external sources referenced are provided for general educational purposes only. For current, accurate information tailored to your specific situation, please always contact us directly for help with your important insurance decisions. We’ll ensure you have the most up-to-date policy details and guidance.