Related reading

I’ve had this conversation dozens of times.

A client gets engaged. The ring cost HK$20,000 or more. They want to protect it. They search “engagement ring insurance Hong Kong” and assume they need a standalone engagement ring insurance policy.

Then they call me and say: “I don’t need home contents insurance. I just want to insure the ring.”

I understand the logic. You’re focused on one specific item. You want targeted protection. Why pay for coverage you don’t need?

But here’s what I’ve learnt after years of helping people protect their valuables in Hong Kong: standalone valuables insurance often costs more than a combined home contents policy that includes your ring. And you miss out on protection you didn’t realise you needed.

Let me walk you through what I’ve seen work, what doesn’t, and how to make sure you’re getting the best value for your money.

The Standalone Valuables Insurance Trap

Standalone engagement ring insurance exists. You can insure just your engagement ring.

The problem is the price.

When you buy standalone engagement ring insurance cover, insurers see higher risk. You’re insuring a portable, high-value item that can be lost, stolen, or damaged anywhere in the world. There’s no broader relationship with you as a customer. The insurer doesn’t know your claims history or risk profile beyond this one item.

So they charge accordingly.

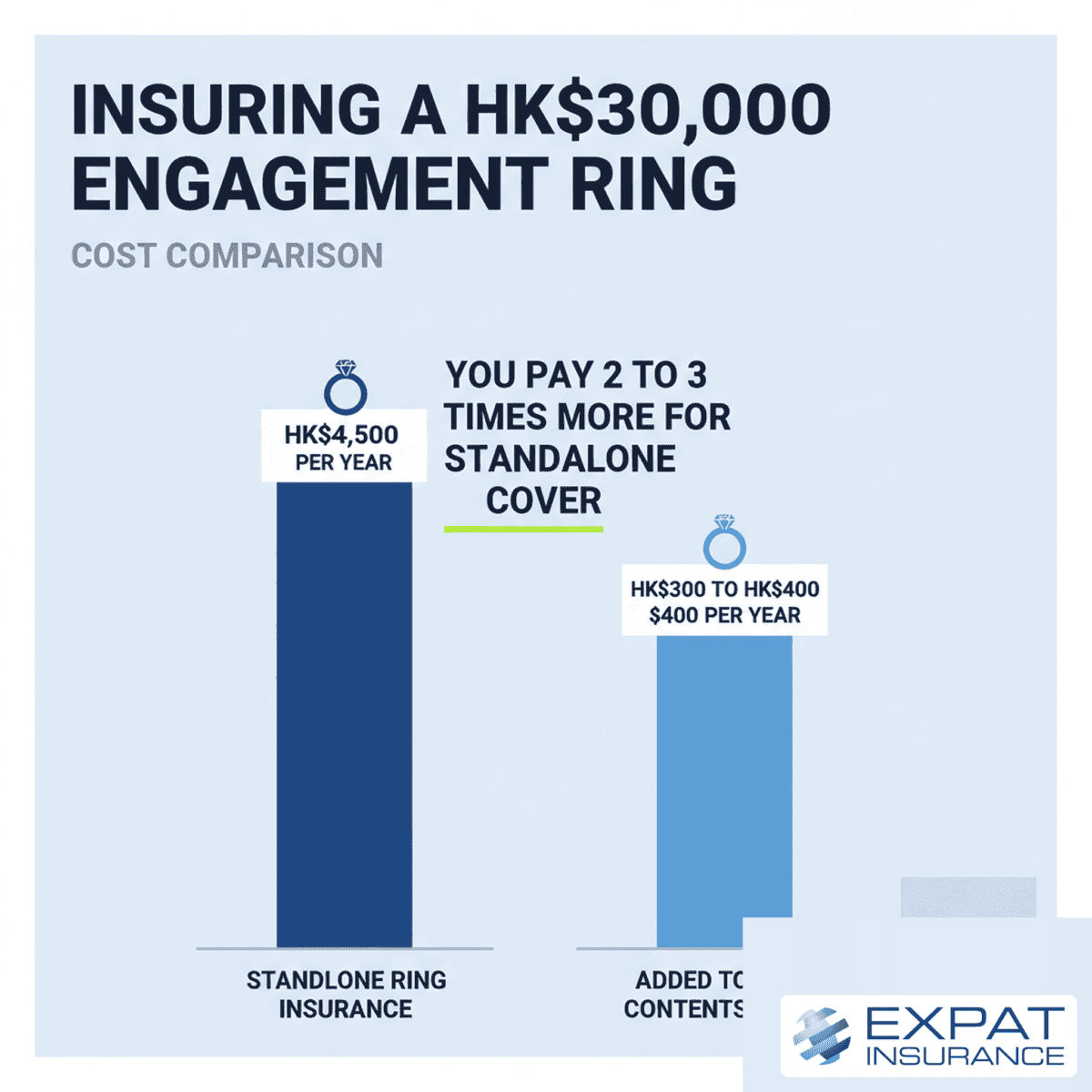

I’ve seen standalone engagement ring insurance policies cost 3% to 5% of the ring’s value annually. For a HK$20,000 ring, you’re looking at HK$600 to HK$1,000 per year. For a HK$50,000 ring, you could pay HK$1,500 to HK$2,500. And there is usually a minimum premium, typically starting at around HK$4,500.

Compare that to adding the ring as a specified item on a home contents policy. The incremental cost is typically HK$300 to HK$400 per year for the same ring, depending on the insurer and your overall coverage.

You’re paying two to three times more for standalone cover.

And you’re not getting better protection. You’re getting less.

What Home Contents Insurance Actually Covers

Most people think home contents insurance is for furniture and electronics.

They don’t realise it covers far more than that.

A standard home contents policy in Hong Kong protects your possessions against theft, fire, water damage, and accidental damage. This includes clothing, kitchenware, books, sports equipment, and personal items.

But here’s where it gets interesting for engagement rings.

Standard policies include some jewellery cover, usually with a single-item limit of HK$10,000 to HK$20,000. If your ring is worth less than that limit, it’s already covered under a basic contents policy. You don’t need anything extra.

If your ring exceeds that limit, you add it as a specified item. You provide a valuation, pay a small additional premium, and the ring is covered worldwide for loss, theft, and accidental damage.

The coverage is identical to standalone engagement ring insurance. But the cost is significantly lower because the insurer is already covering your home contents. The ring is just one more item on the policy.

According to research on insurance bundling, having a combined buildings and contents insurance policy often works out cheaper than taking out separate policies, with some consumers saving more than HK$1,800 annually by bundling their coverage. For a fuller breakdown, see our home contents insurance premiums guide.

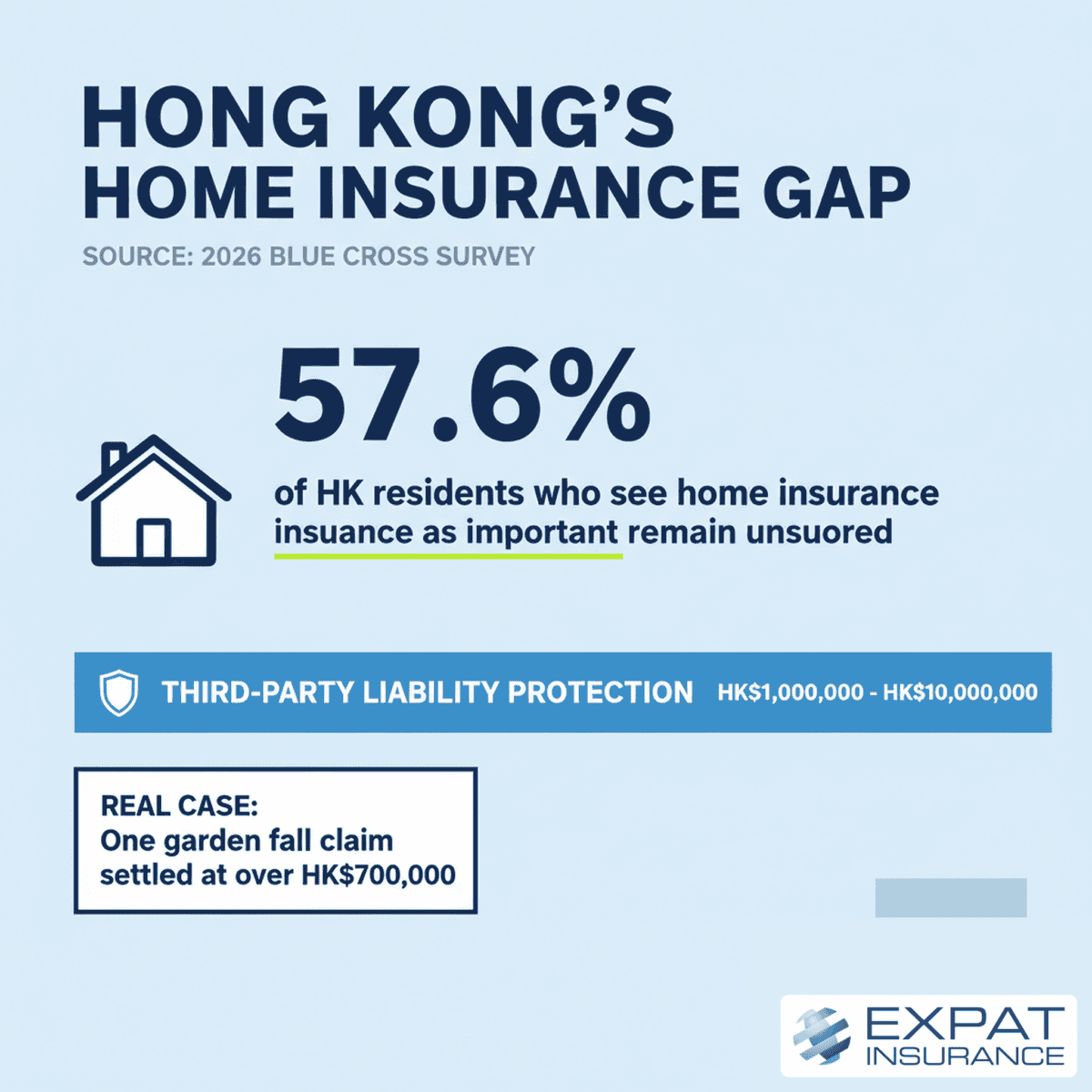

of Hong Kong residents who recognise home insurance as important remain uninsured (Blue Cross, 2026 survey) — many renters wrongly assume a landlord’s policy covers their possessions and liability.

The Hidden Benefit Most Renters Miss

If you rent your home in Hong Kong, you might think you don’t need contents insurance.

Your landlord has insurance, right?

Yes. But landlord insurance covers the building and the landlord’s liability. It doesn’t cover your possessions. And it doesn’t cover your liability to others.

This is where home contents insurance becomes essential, even if you’re renting.

Most home contents policies include third-party liability cover.

This protects you if someone is injured in your home, or if you accidentally cause damage to someone else’s property. The coverage typically ranges from HK$1 million to HK$10 million, depending on the policy.

Let me give you a real example.

You’re hosting friends at your flat in Mid-Levels. Someone trips on a loose tile in your bathroom and breaks their wrist. They can’t work for two months. They need surgery. The medical bills and lost income add up to HK$150,000.

Without liability cover, you’re personally responsible for those costs.

With home contents insurance, your third-party liability cover handles the claim. You pay the excess (usually HK$1,000 to HK$2,000) and the insurer covers the rest.

I’ve seen liability claims in Hong Kong reach hundreds of thousands of dollars. One case involved a tenant whose guest fell down steps in the garden and broke their knee. The claim settled at more than HK$700,000.

According to a 2026 survey by Blue Cross, more than half (57.6%) of Hong Kong residents who recognise home insurance as important remain uninsured. Many renters wrongly assume their landlord’s insurance covers all damages, but landlord policies usually only cover the building itself, not tenant-caused damages or possessions.

You’re exposed to significant financial risk without realising it.

How the Numbers Actually Work

Let me show you what this looks like in practice.

Scenario 1: Standalone Engagement Ring Insurance

You insure a HK$30,000 engagement ring with a standalone engagement ring insurance policy.

Annual premium: HK$4,500

Coverage: Ring only, worldwide

Liability protection: None

Other possessions: Not covered

Scenario 2: Home Contents Insurance with Specified Valuables

You buy a home contents policy covering HK$300,000 of possessions and add the HK$30,000 ring as a specified item.

Annual premium: HK$1,200 to HK$1,800 (total for contents + ring)

Coverage: All possessions, ring covered worldwide

Liability protection: HK$2 million to HK$10 million

Additional benefits: Temporary accommodation if your home becomes uninhabitable, and usually some personal belongings cover outside the home

You’re paying HK$2,700 to HK$3,300 more per year in Scenario 1. And you’re getting:

Protection for all your possessions (appliances, clothing, furniture, kitchen items)

Liability cover worth millions of dollars

Additional living expenses if you need to move out temporarily

The incremental cost for the ring itself? About HK$300 to HK$400.

You’re paying less for ring coverage and getting comprehensive protection for everything else.

Decision Guide: Which Cover Fits You?

- ✔ Ring under your policy’s single-item limit? It may already be covered — confirm the limit.

- ✔ Ring above the limit (e.g. HK$15,000 vs HK$10,000 cap)? Specify it as a named item.

- ✔ Renting in Hong Kong? A contents policy adds vital third-party liability cover.

- ✔ Only want the ring insured? Compare the maths — bundled usually wins.

What About Single-Item Limits?

Standard home contents policies include automatic jewellery cover, but with limits.

Most Hong Kong insurers cap single items at HK$10,000 to HK$20,000 at home, unless you specify them separately. Many policies exclude accidental loss or damage when items are taken outside the home, or cover them with very low limits (e.g. HK$5,000).

This is commonly overlooked.

If your engagement ring is worth HK$15,000 and your policy has a HK$10,000 single-item limit, you’re underinsured by HK$5,000. If the ring is stolen, you’ll only receive HK$10,000.

The solution is straightforward. You specify the ring on your policy.

You provide a valuation certificate from the jeweller or an independent appraiser. The insurer adds the ring as a named item with its own sum insured. You pay a small additional premium based on the ring’s value.

Now the ring is fully covered, usually with no single-item limit and no geographic restrictions. You can wear it anywhere in the world and it’s protected. Our guide on why home insurance fails on valuables explains this trap in more detail.

Why This Matters More Than You Think

I’ve noticed something interesting about engagement ring insurance.

It’s often a gateway to broader financial protection.

Research shows that 50% of people who insure their engagement ring go on to insure other pieces of fine jewellery. But more importantly, buying that first policy opens a conversation about risk and protection.

You start thinking about what else you own that’s valuable. Not just in monetary terms, but in terms of what would be difficult or impossible to replace.

Family heirlooms. Electronics you use for work. Musical instruments. Camera equipment. Watches. Designer handbags.

A home contents policy may cover all of this (with certain limits for specific categories of items). And when you add up the replacement cost of everything you own, you realise the value is significant.

Most renters in Hong Kong underestimate the total value of their possessions. They think about rent and assume their belongings aren’t worth much. Then they list everything out and discover they own HK$200,000 to HK$400,000 worth of stuff.

Contents insurance for renters is relatively affordable, starting around HK$700 per year. For most renters, you’re looking at HK$500 to HK$1,500 per year. The protection is extremely accessible compared to potential losses.

According to the latest Hong Kong Police Force statistics, 816 burglary cases were recorded in 2025, representing the lowest figure since records began in 1969. Whilst Hong Kong maintains exceptionally low crime rates compared to international standards, theft and property damage remain genuine risks to valuable possessions that warrant protection.

The Liability Question Nobody Asks

Here’s what I find most people don’t realise about liability insurance.

Your potential liability is essentially unlimited.

If someone is seriously injured or dies as a result of your negligence, and you’re found legally liable, the claim could run into millions of dollars.

Medical expenses, lost income, ongoing care costs, pain and suffering — these add up quickly.

I’ve seen cases where someone’s guest slipped on a wet floor and suffered a serious back injury. The claim exceeded HK$500,000. I’ve seen cases where a fire started in a tenant’s flat and spread to neighbouring units, causing millions in damage.

Without liability insurance, you’re personally responsible for paying these claims.

With home contents insurance, your third-party liability cover steps in. The insurer investigates the claim, handles the legal process, and pays any settlement or judgment up to your policy limit.

This protection alone justifies the cost of a contents policy, even if you don’t care about insuring your possessions.

And here’s the part that surprises people: liability cover applies whether you own or rent your home.

Your landlord’s insurance doesn’t cover your liability to third parties. That’s your responsibility. If you cause damage or injury, you’re liable.

A home contents policy with liability cover protects you from this risk. And it costs far less than defending a liability claim out of pocket.

How to Get This Right

If you’re purchasing engagement ring insurance in Hong Kong, here’s what I recommend.

Step 1: Get a valuation

Ask your jeweller for a valuation certificate when you buy the ring. This document states the replacement value and describes the ring in detail (metal type, stone quality, carat weight, design features).

If you didn’t get a valuation at purchase, get one now. Independent appraisers in Hong Kong charge HK$500 to HK$1,500 depending on the complexity of the piece.

Step 2: Review your current insurance

If you already have home contents insurance, check your policy document. Look for the single-item limit for jewellery. If your ring exceeds that limit, contact your insurer to add it as a specified item.

If you don’t have contents insurance, get quotes for a policy that covers your possessions and includes the ring as a specified item.

Step 3: Compare the real cost

Get a quote for standalone engagement ring insurance. Then get a quote for home contents insurance with the ring specified.

Compare not just the premium, but what you’re getting for that premium. Factor in liability cover, coverage for other possessions, and additional benefits like temporary accommodation.

In most cases, the home contents policy offers better value.

Step 4: Understand the excess structure

Most policies have an excess (the amount you pay out of pocket when you make a claim). For jewellery claims, the excess typically ranges from HK$500 to HK$2,000, or a percentage of the sum insured.

Make sure you’re comfortable with this amount. A lower premium with a HK$5,000 excess might not be the best choice if you can’t afford to pay that much if you need to claim.

Step 5: Read the exclusions

Every insurance policy has exclusions. Common ones for jewellery include:

Unexplained loss or mysterious disappearance

Wear and tear or gradual deterioration

Loss of stones from their settings unless the entire item is lost

Damage during professional cleaning or repair

Understand what’s not covered so you’re not surprised if you need to claim.

What This Means for You

Protecting your engagement ring with the right engagement ring insurance doesn’t have to be complicated or expensive.

The key is understanding your options and choosing coverage that makes sense for your situation.

If you’re renting in Hong Kong and you think you don’t need home contents insurance, reconsider. The liability protection alone is worth the premium. The coverage for your possessions is a bonus.

If you’re comparing standalone valuables insurance to a combined contents policy, do the maths. Factor in everything you’re getting, not just the ring coverage.

And if you’re not sure what you need, talk to someone who can explain your options without pushing you towards a specific product.

That’s what we do at Expat Insurance.

How You Get the Engagement Ring Protection You Need

Home contents insurance doesn’t have to be complicated. At Expat Insurance, I help you understand exactly what you’re buying and make sure your policy protects what matters most to you.

No pushy sales tactics. We have a friendly conversation, show you the lay of the land, and explain the different options available. You move forward at your own pace. People choose to work with us because we educate them on their options and help them feel confident about what will work best for them.

I’ll walk you through the valuation process so you’re not caught by the underinsurance trap. I’ll explain the excess structure so you know what you’ll pay out of pocket for different claim types. And I’ll help you navigate the documentation requirements, whether you’re in a high-rise flat or a village house. You can start by reading our engagement ring insurance cost guide.

My goal is straightforward. I want you to have home contents insurance coverage that works when you need it.

Get in touch with us today. We’ll review your situation, answer your questions, and help you find a policy that provides the protection you need at a price that makes sense.

How We Work With You

Step 1: We Talk and Answer Your Questions

When you get in touch, we’ll explain who we are, what we do, and most importantly, what we’re going to do for you specifically. We’ll answer any questions you have about home contents insurance and engagement ring insurance cover.

Step 2: We Educate You on Your Options

We’ll research the market and come up with quotes and options tailored to your situation. Whether you’re in a village house, an older building, or a standard flat, we’ll find insurers willing to provide the coverage you need. We’ll take you through each option so you understand what’s available.

Step 3: You Decide What Works Best

We’ll meet with you in person or speak on the phone to discuss your options. We’ll explain the differences between policies, help you understand the excess structures, and make sure you’re comfortable with everything. The choice is yours. We’re here to help you make an informed decision.

Step 4: We Stay With You

Once your policy starts, we’re here to help. We’ll meet with you at least once a year to review your coverage, discuss any changes in your situation, and consider any additions you’d like to make. Your needs change over time, and your home contents insurance should change with them.

Ready to protect your engagement ring and everything else that matters? Get in touch with us today.

Speak with us today

No pushy sales — just a friendly conversation about protecting your engagement ring and everything else that matters. We’ll review your situation and explain your options clearly.

https://expatinsurance.com.hk/contact/

Phone: +852 3563 9771

Office Location: Suite 701, Connaught Commercial Building, 185 Wan Chai Road, Wan Chai, Hong Kong

Email: [email protected]

This article references information from the following sources:

- Zurich Insurance Hong Kong — Home Insurance

- AXA Hong Kong — Home Contents Insurance

- Chubb Hong Kong — What Does Home Insurance Cover

- MSIG Hong Kong — Home Insurance Products

- Insurance Authority Hong Kong — Consumer Information

- Hong Kong Police Force — Crime Statistics

Disclaimer: Insurance products, terms, and conditions may change over time. Website content and linked resources may be updated or become out of date. Please always contact us directly for current information and personalised advice regarding your important insurance decisions.