Your mortgage lender requires building insurance(1). You purchase a policy. You assume you’re protected.

This assumption costs property owners thousands—sometimes hundreds of thousands—when disaster strikes.

We’ve spent years helping property owners understand Hong Kong building insurance, and the gap between what people think they have and what they actually need remains one of the most dangerous blind spots in property ownership. Many policyholders are underinsured(2), whilst some are overinsured.

The problem isn’t that people don’t care about protection. The problem is that they’re protecting the wrong thing with their Hong Kong building insurance.

The Three Numbers That Confuse Everyone

Related reading

- Our Building (Fire) Insurance service page — full overview of coverage we arrange.

- Fire Insurance Trap

When you think about your property’s value, three fundamentally different numbers exist:

Market value is what you paid for the property. It includes the building, the land, location premium, supply and demand factors, and the developer’s profit margin if you bought new construction.

Rebuilding cost is the actual cost of materials and labour to reconstruct that specific structure. When you rebuild, you’re not paying for location or market conditions. You’re paying construction costs.

Mortgage amount is what you borrowed from the bank—typically a percentage of the market value after your deposit.

Your bank only cares about protecting the money they lent you. That’s why they require building insurance matching your mortgage amount. In Hong Kong, when you apply for a mortgage, banks will require you to purchase fire insurance(3) (building structure insurance) because the property serves as collateral for the loan.

But here’s what catches people off guard: your mortgage amount may be significantly more or significantly less than your actual rebuilding cost.

Why Market Value Creates Dangerous Assumptions

The biggest misconception we encounter is property owners insuring for market value. This seems logical—you paid HKD 10 million for your property, so you insure it for HKD 10 million.

In most cases, this means you’re overinsured. Market value also includes the land (or location), which can represent a substantial portion of your property’s worth. When you rebuild after total loss, the land is already there and the property will presumably be rebuilt in the same location. You’re only replacing the structure.

Rebuilding cost typically runs lower than market value because it strips away all the market premium—the desirable neighbourhood, the school catchment area, the trendy postcode.

The reverse creates the more dangerous scenario. Some property owners assume insuring for their mortgage amount provides adequate building insurance protection. If your mortgage represents 80% of market value and your rebuilding cost sits at 60% of market value, you’re probably fine. But if your mortgage sits well below your actual rebuilding cost, you’re financially exposed.

When Rebuilding Costs Exceed Market Value

Whilst uncommon, situations exist where rebuilding actually costs more than market value.

This happens in less attractive areas where the gap between construction costs and market value narrows. Imagine a scenario where labour and material costs spike due to high demand, but market values in that particular neighbourhood stagnate because people are moving away.

You’re left holding a property that costs more to rebuild than buyers will pay.

The Rebuild Cost Calculation Challenge

Determining accurate rebuilding cost for your Hong Kong building insurance proves remarkably difficult.

You can purchase this information from specialist companies or use online calculators. But any calculation remains a best estimate.

Your calculation becomes outdated quickly.

Do your best to estimate rebuilding cost based on available data, your home’s size, and your property’s grade—low, medium, or luxury. A basic property using simple materials won’t cost the same to rebuild as a luxury home featuring imported Italian marble. This estimate becomes the foundation for your building insurance coverage.

The Solution That Removes Guesswork

An alternative approach eliminates the estimation challenge entirely.

Some insurers in Hong Kong offer building insurance that charges a fixed premium based on your property’s size and age but guarantees to pay the actual rebuilding cost or your outstanding mortgage amount at the time of loss.

This removes the burden of estimating rebuilding costs and adjusting your sum insured annually for inflation or mortgage reduction. Banks typically charge a service fee every time you change your building insurance sum insured, making annual adjustments prohibitively expensive.

For 95% of cases, this guaranteed replacement approach to building insurance proves worthwhile.

The limitations? Not many insurers offer this structure. If you have a very small mortgage or exceptionally low rebuilding costs, you may overpay in premium. Properties older than 50 years typically don’t qualify—presumably due to higher risk and uncertainty around older construction methods and materials.

Hidden Factors That Inflate Rebuilding Costs

Even accurate rebuilding cost calculations miss critical factors that emerge during actual reconstruction.

Current building codes create the largest and most frequent source of building insurance underinsurance. When you rebuild, you must comply with modern standards—updated electrical systems, environmental compliance, sprinkler systems, improved insulation—even if your original structure was built decades ago.

These changes may significantly increase rebuilding costs beyond what a standard rebuilding cost calculation tells you.

Construction input prices can rise sharply due to supply and demand, as well as global factors such as trade wars or supply chain disruptions. This volatility means even recent calculations become outdated rapidly.

Policy Exclusions That Surprise Homeowners

Exclusions like war or nuclear fallout exist in building insurance policies. You’re unlikely to face these scenarios. But if you do, you’re facing total loss with no coverage.

More realistic concerns centre on water damage and typhoon-related damage in Hong Kong. Hong Kong building insurance policies typically cover damage from typhoons, heavy rainfall, and burst water pipes, but coverage terms vary significantly between insurers.

The Tai Po case last year demonstrated complexity at scale—several towers burnt down simultaneously. The claims process stretched on as insurers assessed all claims and determined liability. When third parties bear responsibility, insurers pursue those entities to recover losses, extending the timeline before you receive settlement.

What Property Owners Get Wrong During Claims

You should examine excess terms carefully. They vary dramatically between insurers, particularly for water damage claims.

For the same property, we’ve seen policies ranging from nil excess to HKD 10,000 or 10% of the claim amount, whichever is higher.

That difference becomes substantial on a HKD 500,000 water damage claim. One policy pays the full amount. Another requires you to cover HKD 50,000 yourself.

Most property owners don’t compare excess terms when purchasing Hong Kong building insurance coverage. They focus on premium costs and coverage limits, missing this critical detail that determines your out-of-pocket expense when you actually need to claim.

The Responsibility Gap

Here’s the uncomfortable truth: it’s your responsibility, not your insurer’s, to ensure you have adequate Hong Kong building insurance coverage.

Far too many homeowners have no idea what rebuilding their home would actually cost. Many homeowners simply buy the coverage amount their bank suggests to cover their mortgage.

That suggestion often isn’t enough.

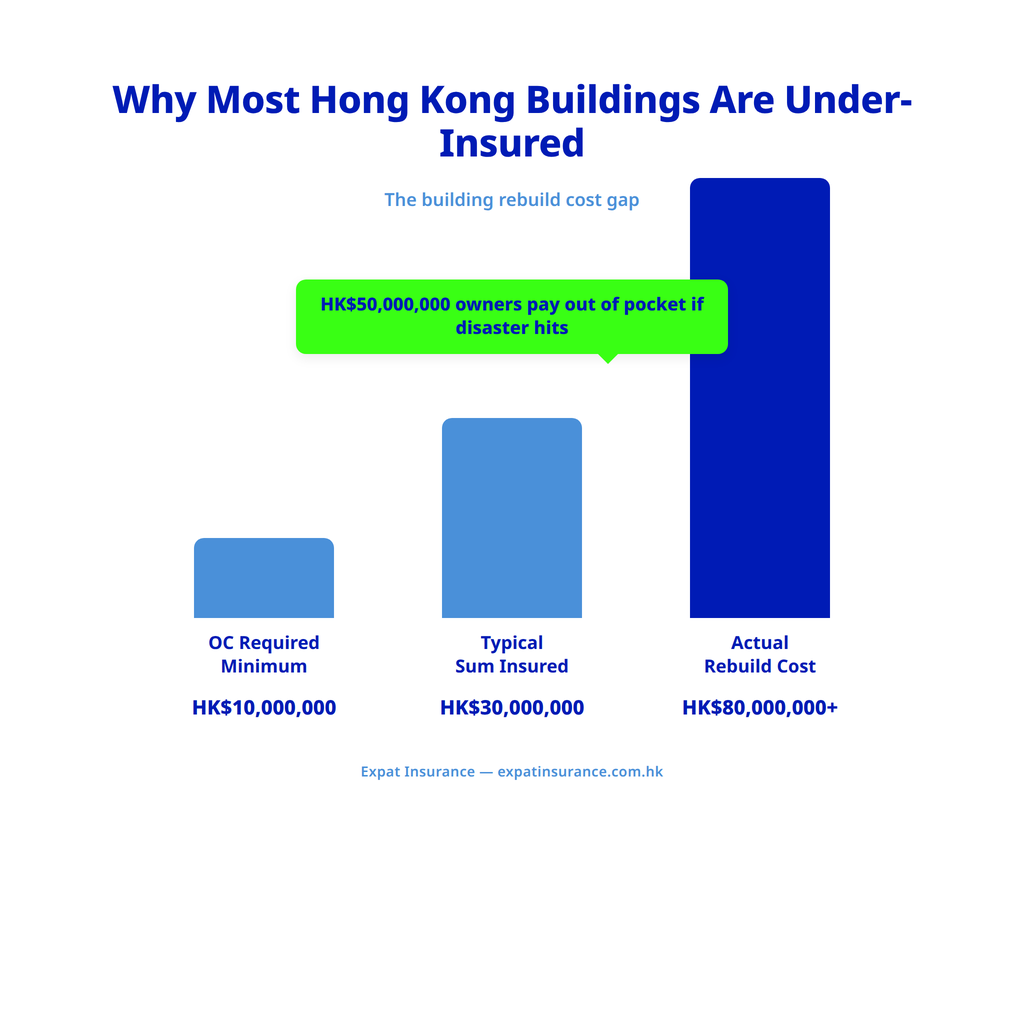

Over two-thirds of homes are currently underinsured. And there is a growing disconnect between property values and actual reconstruction costs.

Building a Proper Protection Strategy

Start by obtaining a professional rebuild cost assessment. Specialist companies provide detailed evaluations based on your property’s specific characteristics.

- Structural damage from fire

- Typhoon and storm damage

- Water ingress (sudden)

- Common areas liability

- Subsidence (with rider)

- Demolition + debris removal

- Gradual settlement

- Vermin / insect damage

- Tenant contents

- War, nuclear, contamination

- Faulty workmanship

- Vacant property over 30 days

Review your Hong Kong building insurance policy annually. The Investor and Financial Education Council (IFEC) Hong Kong advises that you should always check whether your assets have increased in value when renewing your insurance to ensure adequate cover. Construction costs, building codes, and your property’s features change. Your coverage needs to keep pace.

Consider guaranteed replacement cost coverage in your building insurance if your property qualifies. This provides whatever is needed to replace your home in its original condition.

Document your property thoroughly. Photograph every room, major systems, finishes, and custom features. Store this documentation off-site or in cloud storage. When you need to claim, detailed records support accurate settlement.

Understand your excess structure across different claim types. Water damage, storm damage, and fire may carry different excess amounts.

Don’t assume your mortgage-required building insurance coverage protects you adequately. It protects your lender. Your job is protecting yourself.

Why This Matters Now

Building insurance isn’t just about satisfying your mortgage lender. It’s about protecting your most significant asset from devastating financial loss.

The gap between what people think they have and what they actually need continues to widen. Construction costs rise faster than property values in many markets abroad; this may become true in Hong Kong as well. Building codes become more stringent. Climate-related risks increase.

You can either address these realities proactively or discover them when you’re standing in front of your damaged property, realising your coverage falls HKD 1,000,000 short of what you need to rebuild.

At Expat Insurance, we help property owners understand their actual coverage needs and find policies that provide genuine protection. The premiums we quote match what insurers offer direct buyers, but our strong relationship with insurers often means we can negotiate better terms and conditions.

Should you need to claim, Expat Insurance will assist with the claims process and negotiate settlement with the insurance company when necessary.

Your building insurance should protect your property, not just your lender’s interest. Make sure you understand the difference.

How You Get The Protection You Need

Hong Kong building insurance doesn’t have to be complicated. At Expat Insurance, we help you understand exactly what you’re buying and make sure your policy protects what matters most to you.

No pushy sales tactics. We have a friendly conversation, show you the lay of the land, and explain the different Hong Kong building insurance options available. You move forward at your own pace. People choose to work with us because we educate them on their options and help them feel confident about what will work best for them.

We’ll walk you through the rebuild cost assessment process so you’re not caught by the underinsurance trap. We’ll explain the excess structure so you know what you’ll pay out-of-pocket for different claim types. And we’ll help you navigate coverage options, whether you need guaranteed replacement cost coverage or a straightforward policy based on your property’s specifications.

Our goal is straightforward. We want you to have building insurance coverage that works when you need it.

Get in touch with us today. We’ll review your situation, answer your questions, and help you find a policy that provides the protection you need at a price that makes sense.

How We Work With You

Our process is straightforward and designed around your needs.

Step 1: We Talk and Answer Your Questions

When you get in touch, we’ll contact you for a friendly conversation. We’ll explain who we are, what we do, and most importantly, what we’re going to do for you specifically. We’ll answer any questions you have about Hong Kong building insurance.

Step 2: We Educate You on Your Options

We’ll research the market and come up with quotes and options tailored to your situation. Whether you need guaranteed replacement cost coverage, standard sum insured policies, or specialist coverage for older properties, we’ll find insurers willing to provide the coverage you need. We’ll take you through each option so you understand what’s available.

Step 3: You Decide What Works Best

We’ll meet with you in person or speak on the phone to discuss your options. We’ll explain the differences between policies, help you understand the excess structures and coverage limits, and make sure you’re comfortable with everything. The choice is yours. We’re here to help you make an informed decision.

Step 4: We Stay With You

Once your policy starts, we’re here to help. We’ll get in touch with you at least once a year to review your coverage, discuss any changes in your property or mortgage situation, and consider any adjustments you’d like to make. Your needs change over time—property improvements, inflation, mortgage reductions—and your building insurance should change with them.

Speak with us today

No pushy sales. Just a friendly chat about your options.

+852 3563 9771 · [email protected]

Suite 701, Connaught Commercial Building, 185 Wan Chai Rd, Wan Chai

expatinsurance.com.hk/contact

Sources

- Hong Kong Insurance Authority — mandatory fire insurance for mortgaged property

- South China Morning Post — Hong Kong property underinsurance reporting

- Hong Kong Insurance Authority — mortgage fire insurance requirement

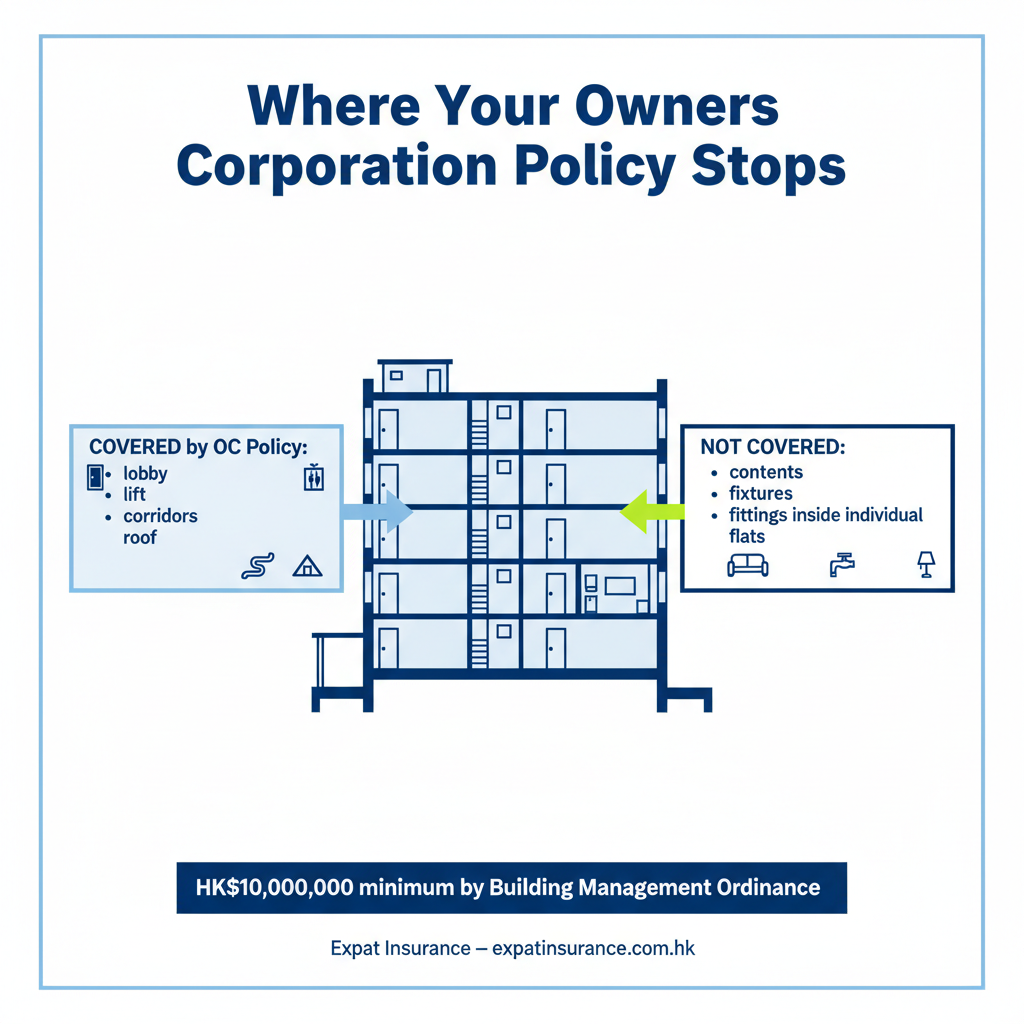

- HK Building Management Ordinance — Cap 344, OC HK0M minimum insurance

- Hong Kong Insurance Authority — older building underinsurance data

- Hong Kong Observatory — typhoon and severe weather data

Information in the insurance industry changes frequently. Linked content may change or become outdated. Please always contact us for help with your important insurance decisions.